The Apple Event never fails to get the internet talking, but just to be safe, Apple used the hashtag #AppleEvent, sponsored a custom hashtag emoji and touted a promoted tweet on Twitter this year for more marketing moxie. The annual fall event was livestreamed across AppleTV, iOS devices and on Microsoft’s new browser, Edge, a nice subtle way of wooing Android users to the platform. Recently named the world’s most valuable portfolio, Apple pulled out all of the stops for this year’s announcements—or lack thereof if you’re part of a legion of shunned MacBook professionals in desperate need of an upgrade. So let’s get to it.

iPhone 7

It was no surprise that the iPhone 7 was officially introduced on Wednesday, with pre-orders available beginning Friday. The 32GB iPhone 7 will retail for $649 (the same starting price as the iPhone 6) and $769 for the 32GB iPhone 7 Plus. Public service announcement: be a decent human and don’t do anything that will shame the progress of mankind.

The iPhone 7 features two rear cameras and live previews of camera shots with a shallow depth of field. Photos taken on the iPhone 7 Plus will be able to achieve a very sharp foreground and blurry background for all those artistic shots of the chicken Caesar salad you’ll surely incessantly snap during lunch. The new phone may look an awful lot like the iPhone 6, but there is one notable difference—the absence of a headphone jack. Keep reading before your heart explodes.

Apple introduced the AirPod wireless headphones that can be paired to the device with the touch of a button. Each iPhone 7 will ship with the wireless AirPods and a Lightning-to-3.5-millimeter headphone jack adapter. If you want the headphones by themselves, they’ll cost you a cool $159 when they become available this October. If that’s still music to your ears, let’s move on to . . .

Nike+ Apple Watches (Source: Apple)

Watch Out(side)

The new Apple Watch appears to be the same aesthetically but features built-in GPS and is water-resistant up to 50 meters, which means it will track swim activity, which really means you can be the next Michael Phelps by the 2020 Olympics, or Ryan Lochte if you only have plans to abuse and misuse it.

A strategic partnership with Nike resulted in a special Apple Watch designed for fitness. The Nike+ version is aimed at runners and will “hit the road”—and your bank account—in late October for $369. The first Apple Watch focused heavily on fitness; the Nike+ version includes many health apps as well as calories burned and mileage and step tracking. Compared to previous versions, Apple has added several new features with the athlete in mind including water resistance for swimming, built-in GPS and a brighter display for daytime activities.

Ninten-DO on the Ninten-GO

Super Mario Run is a new game headed to iOS devices this holiday season, starring the world’s most famous plumber—sorry for the snub Thomas Crapper! Shigeru Miyamoto, creator of Super Mario Brothers, took to the stage and demonstrated the colorful, one-handed gameplay design, which features multiplayer and the chance to customize your very own Mushroom Kingdom. In addition to Mario’s mushroom-stomping marathon, Pokémon GO will be available for Apple Watch by the end of 2016, allowing players to access game features without having to pull out their phones. What a time to be alive!

Apple has teamed up for a “super” new app, bringing Nintendo’s most famous character to iOS. Super Mario Run is an endless runner launching this holiday season in which the iconic video game character automatically runs to the right. Players can tap and hold the screen to make Mario jump, avoid obstacles or hit objects—all while completing as many levels as they can and racking up points. Super Mario Run will also feature “Toad Rally,” a multiplayer mode where players can compete against their friends for the high score, which is earned by collecting coins and impressing Toad characters with “daring moves.” Players can then use their performance to customize their very own Mushroom Kingdom.

The game was presented on Wednesday at the 2016 Apple Event by Super Mario Brothers creator, Shigeru Miyamoto who demonstrated the colorful, one-handed gameplay design.

“Super Mario has evolved whenever he has encountered a new platform, and for the first time ever, players will be able to enjoy a full-fledged Super Mario game with just one hand, giving them the freedom to play while riding the subway or my favorite, eating a hamburger,” said Miyamoto.

Super Mario Run does not yet have a price point, but it will be fixed and not the popular “freemium” model, i.e. you will not be prompted to buy in-game items. iOS users will be able to download and enjoy a portion of Super Mario Run for free and will be able to enjoy all of the game content available in this release after paying a set purchase price,” Nintendo stated in a press release.

The title has already appeared in the App Store for users to receive notifications for when the game becomes available. Apple will also release Mario stickers in iMessage for iOS 10 alongside the game’s release. If you don’t have an iOS device, don’t cry in your mushrooms just yet—“We do intend to release the game on Android devices at some point in the future,” Nintendo confirmed.

For those who just can’t get enough of Nintendo on iOS, Niantic’s mobile darling, Pokémon GO will soon be available on Apple Watch by the end of 2016.

“With Pokémon GO on Apple Watch, I will never miss a PokéStop,” said John Hanke, CEO and founder of Niantic. Unlike other versions of the break-out hit, Apple Watch users will not have to break out their phones to interact with the game. According to Hanke, Pokémon GO has already been downloaded 500 million times on iOS, and players have walked 4.6 billion kilometers while playing the game. The Apple Watch version will not only allow players to collect creatures along their path, but it will track their steps and calories burned in real time, too.

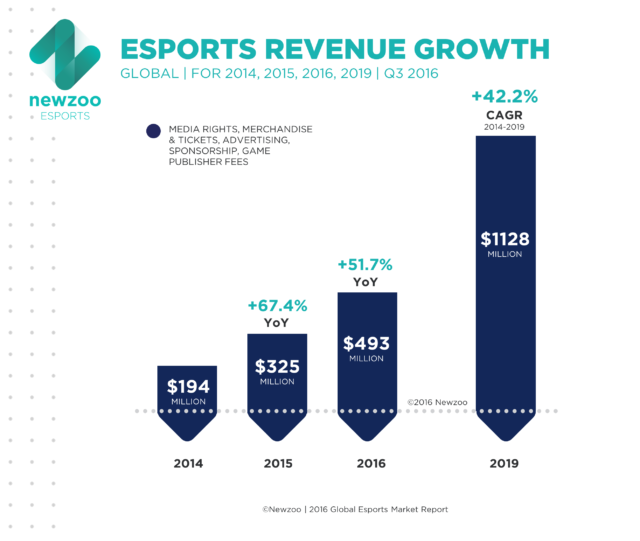

Market research firm Newzoo has revised its eSports revenues forecast for 2016, bumping its projection from $463 million to $493 million (a $30 million difference). Taking into account this adjustment, Newzoo’s latest market report pegs the rate of eSports revenue growth at a remarkable 51.7 percent year-on-year.

The revision has been made in response to a wave of publisher investment in the burgeoning eSports arena, as well as the accelerating uptake of the media rights business model that Newzoo anticipates as a key driver of future growth. It’s this shift from direct advertising income to media partnerships that the company believes will propel eSports to $1.1 billion of revenue in 2019.

Publisher Investment

All of which is to say that eSports revenues are growing even faster than expected, and that’s largely been driven by an increase in publisher investment, as an increasing number of companies look to eSports as a means to expand their audiences and boost engagement among existing players. Tournaments and competitions have emerged as a key site of publisher interest, with prize pools often standing at millions of dollars.

It’s not just competitors that benefit from these big money events though – it’s created an opportunity for third-party event organisers, too. Newzoo estimates that publishers will have spent somewhere in the region of $100 million on these service providers by the year’s end.

The firm’s report notes that publisher investment is unlikely to continue growing at this rapid rate over the coming years as the number of companies entering the arena shrinks. Instead, Newzoo expects eSports growth to be driven by a significant increase in revenues from brands.

Media Rights

ESports revenues from advertising, sponsorships and media rights are already considerable, and Newzoo believes that they’ll reach $350 million for 2016. But there’s still plenty of room for growth in this arena—even if the rate of publisher investment begins to plateau—and the firm notes that the investment by brands expressed on a per fan basis is still several times lower than you see in traditional sports.

Even at present levels, investment by brands still represents 71 percent of the “eSports economy,” with the still sizable remainder generated by consumer purchases of event tickets and merchandise or publisher spending on service providers.

The report anticipates that the percentage of eSports revenue represented by brand investment is only set to grow as publishers double down on sponsorship and advertising opportunities. And, as the popularity of eSports teams continues to grow, Newzoo expects savvy publishers to begin sharing revenues with these gaming athletes. After all, the fanbases for celebrity gamers may very soon outstrip that of the games they’re competing in.

One of the most important job functions for marketers at all levels is to keep abreast of the latest industry news, trends and metrics. That knowledge not only informs your overall marketing strategy and day-to-day marketing tactics, it’s vitally important for marketers to share critical knowledge across their company. All kinds of decisions about product development, business development and management depends on this knowledge, and marketing is where most businesses look for that info. Even more important is taking in information from a variety of sources as a way to verify important trends and to look for inconsistencies.

One of the leaders in creating development tools for the games industry is Unity, and its enormous user base of developers provides a broad perspective on what’s happening across the games industry. Its latest report, Games By the Numbers Q2 2016, has plenty of useful information. As the report notes, “With 238,248 made with Unity games generating 4.4 billion installs across 1.7 billion unique devices globally in Q2 2016, Unity is uniquely positioned to help understand trends across the greater mobile games industry.”

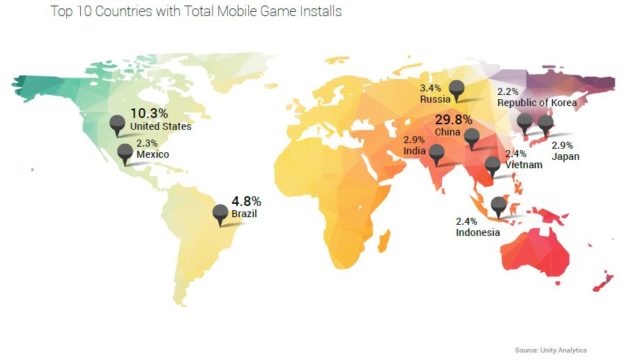

The report details the progress that mobile games are making and the current market conditions around the world. The growth in game installs is being led by the BRIC countries: Brazil, Russia, India and China, who collectively accounted for four of the five top countries for global game installs with 41 percent of the total (42 percent of Android game installs).

Android Fragmentation Continues

One of the biggest issues for Android is the severe fragmentation of the user base, both with the incredible range of devices and the variation in Android operating system versions. Those two factors make it difficult for developers to create games that can work seamlessly across the Android market. Worse, trying to test software across a representative sample of Android devices running different versions of the Android OS can be expensive, difficult and time-consuming. So product developers need to know from marketers just what the Android market currently looks like, so that developers can address the minimum number of different devices and OS versions.

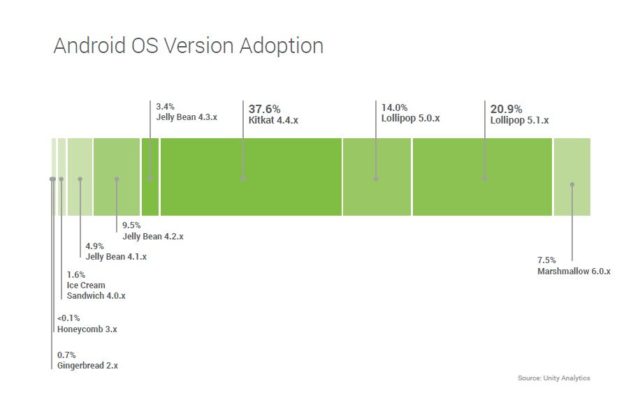

The Android OS fragmentation is clearly an issue, with Marshmallow (Android 6.0.x), the latest version of Android OS, only at a 7.5 percent market share. Version adoption is spread, with Kitkat (Android 4.4.x) at 37.6 percent, Lollipop (5.0.x) at 14 percent, and Lollipop (5.1.x) at 20.9 percent. Android’s latest OS, Nougat, is being released now. Unfortunately, it doesn’t look like the Android OS fragmentation issue will get better any time soon. It seems more likely the situation will continue about the same or even worse. In short, Android 5.0 or above covers over 40 percent of devices, and games that work on Android 4.4 or better may capture nearly 80 percent of the market.

The report also noted that while Samsung led the BRIC Android market with 18.1 percent of game installs and 35.1 percent of the overall market. Other top Android phone makers were all Chinese: Xiaomi, VIVO, OPPO, and Huawei. That correlates with other sources, which show that the growth in the mobile phone market is coming from the lower-end and midrange Android phones. These mobile devices have enough horsepower to do a good job playing games, and lower prices that are attracting a broader audience. Although some lower-cost manufacturers are gaining on Samsung, none of the other companies have risen out of the single digits in market share.

The iOS market has a much cleaner situation, with 78 percent of installs occurring under iOS 9. If you include iOS 8.x’s 12.5 percent share, you’ve got over 90 percent of the iOS device market covered. As far as the hardware goes, iPhones are over two-thirds of game installs. The latest versions of the iPhone (the 6 and 6s models) collectively account for over 36 percent of the iPhones out there, or over half of all the iOS devices.

Geographic Trends: Android Vs. iOS

While Android is clearly dominant in terms of sheer numbers across the world, that dominance varies from place-to-place. Some 96 percent of game installs in Indonesia are on Android; both Korea and Brazil have Android game installs at 92 percent of the total. China saw 81.4 percent of its game installs occur on Android, the US saw 68.8 percent of game installs on Android, and Japan saw only 47 percent of game installs on Android. Overall, 82 percent of global game installs occur on Android and only 17 percent on iOS devices.

The best places for iOS software are clearly China, Japan, and the US. Those three nations combined had 60 percent of iOS game installs worldwide. Beyond that, individual countries are responsible for low single-digit amounts of iOS worldwide game installs, with the UK in fourth position and dropping from there.

The leading countries for Android installs are China (with almost 30 percent), the US (with 8.6 percent) and Brazil (with 5.4 percent), trailing off into low single digits from there. Collectively, all the top 10 countries for Android installs were only 63 percent of total Android game installs, while the iOS top ten countries represented over 75 percent of game installs. Android is just more widely spread than iOS, and there’s no sign that will change in the future.

Summary

The mobile game market continues to increase in size, with Unity alone seeing 238,248 mobile games made with Unity generating over 4.4 billion game installs in the second quarter of 2016, reaching over 1.7 billion unique devices. That’s up from first quarter by 4 percent on unique devices, 6 percent on installs, and 8 percent in the new games available.

Unity is probably responsible for at least one-third of all mobile games out there, and perhaps more. These numbers they’ve shared provide significant insight into the market, and marketers should make sure this information gets shared to the people who need to know.

Tencent is one of the largest investment, internet technology and entertainment companies in the world, with a deep connection to one of the biggest mobile audiences in the world: China. The company is a leading gateway to the massive Chinese user base through multiple channels including the Weixin/WeChat and QQ communication platforms, Qzone for social networking, and the QQ games platform for online games, QQ Music, and much more. For perspective, Weixin/WeChat has over 800 million combined monthly active users while the QQ instant messaging service has nearly 900 million active monthly users.

Today, Tencent and global mobile marketing attribution analytics company AppsFlyer announced a partnership. With it, AppsFlyer becomes the first third-party service to track the effectiveness of app install campaigns on Tencent Social Ads. According to data from AppsFlyer, about 4.4 percent of Chinese app users spend money on in-app purchases (IAP) and spend an average of $12.71 per month. AppsFlyer has tracked over 550 million app installs in China over the past three months alone and found that Asians spend 40 percent more than the rest of the world. Additionally, Chinese networks such as Mobvista, Avazu and others have grown significantly over the past six months.

Ran Avrahamy, marketing VP for AppsFlyer, talks to [a]listdaily about the partnership with Tencent and how it represents a gateway into the massive Chinese market.

Ran Avrahamy, AppsFlyer vice president of marketing

What led to the partnership between Tencent and AppsFlyer?

Tracking and measurement is a core ingredient of almost every successful mobile ad campaign, and Tencent was looking for a trusted, independent third-party global measurement partner that could provide advertisers throughout the world with objective and accurate tracking across its vast media properties. AppsFlyer and Tencent have been working together in different capacities for years, and as both are market leaders in their respective industries in China, once discussions started they moved pretty fast. AppsFlyer works with the largest brands, developers and advertisers both in China and across the globe, and Tencent’s channels are go-to outlets for nearly a billion mobile users in China, so this partnership is a natural, powerful fit. Advertisers now have access to the channels and data they need to conduct smarter, more informed app marketing campaigns that reach the masses in China.

How does AppsFlyer enhance the Tencent Social Ads platform?

AppsFlyer provides tracking and measurement of ads on the Tencent Social Ads platform, which gives advertisers more confidence in the accuracy of their results on one of the largest ad platforms in the world. This in turn allows them to spend greater ad budgets with more confidence—as well as optimize their activities and compare the quantity and quality of traffic coming from Tencent Social Ads with other media sources. And on the optimization front, by using detailed data on install and post-install activities sent by AppsFlyer will enable Tencent advertisers to further optimize their campaigns.

What are the challenges of tracking mobile install campaign effectiveness on so many different channels (WeChat, QQ, QQ Music, etc.)?

There’s always a challenge in tracking install campaigns across so many sources, but that challenge is largely met by having a proper attribution partner. AppsFlyer now measures across more than 2,000 integrated ad networks, so from an integration standpoint, it’s one more integration that an advertiser can easily access through a single dashboard. But this isn’t “just another” integration—it’s a milestone that benefits everyone involved: the advertisers and the media sources alike. It also represents a gateway into the massive Chinese market.

From an advertiser perspective, they’re able to track their campaigns on Tencent Social Ads on one dashboard at a high, aggregate level, as well as on a more granular level, so our dashboard really makes this easy for them as well, especially to measure and compare activities across the different channels. It’s just a matter of marketers keeping an eye on the numbers so that they can optimize their campaigns accordingly.

With 800 million monthly active users on WeChat alone, and 900 million on QQ, how would you characterize a successful campaign compared to one in Western markets?

With Tencent, they have so many users that there’s really no single platform in the West that can really compare, with the exception of Facebook. So the ability to scale quickly obviously exists in a big way, allowing advertisers to attract both a quantity and quality of users throughout China. But at the end of the day, the benchmarks for advertisers will all be fairly similar in terms of performance on different media sources, with marketers focusing on conversion rates, engagement and monetization—and fine-tuning their campaigns to hit their objectives.

What would you say is the most important thing to keep in mind when launching a new mobile campaign on a platform such as Tencent Social Ads?

Probably the most important thing is to keep a close eye on the numbers, especially early on, because there will likely be some surprises. Any time you start advertising on a new platform, it’s important to see what’s working versus what isn’t working and adjust from there. But for Western developers and marketers looking to advertise on Tencent, it’s especially important to measure the effectiveness of certain campaigns because it may require a different creative spin, timing and messaging in order to achieve the desired results and lifetime value of users.

Apple is about to enter the branded content foray with an original reality-competition TV show about iOS app developers. “Planet of the Apps” just wrapped an open call for 100 aspiring tech entrepreneurs and the show itself is scheduled to air in 2017.

Although specific details about the program’s format have yet to be revealed, it appears that “Planet of the Apps” will be a Shark Tank-type program for app ideas, which can then be funded by interested mentor judges.

Lightspeed Venture Partners, which was the first institutional investor in Snapchat and Alba’s Honest Company, has joined the series as a venture capital partner. Lightspeed is committing $10 million to fund the development of the apps selected in “Planet of the Apps”

Mentors and advisors for the project include Hollywood elite like Gweneth Paltrow and Alba. Also on board is musician will.i.am and tech investor Gary Vaynerchuck. Paltrow and will.i.am will also executive produce the project, along with Ben Silverman and Howard T. Owens of Propagate.

“Planet of the Apps” is Apple’s first original TV program and a big move in the direction of branded content. The tech giant was recently named the most valuable brand portfolio in the world, and clearly has no plans of slowing down. The show is scheduled to film this fall, and applicants were required to have an iOS, macOS, tvOS, or watchOS app in a “beta or functional state” by Oct. 21, according to the entry guidelines.

“As a mentor on ‘Planet of the Apps,’ I’m looking forward to meeting entrepreneurs looking to address a problem with an innovative solution, and to help them realize their vision,” Alba said. “I can’t wait to see the ideas the app developers bring to the table.”

Ever since the FTC released its most recent guidelines on native ads, the agency has been cracking down on violations, especially on social media. The guidelines state that native ads must be tagged with “ad” or “sponsored advertisement” for proper disclosure.

When the new guidelines were released in December, Todd Krizelman, co-founder and CEO of tracking and ad analyzing company MediaRadar, revealed that only about 30 percent of sites already complied with the rule and 26 percent of websites run native ads without any sort of mention of the sponsor whatsoever.

Eight months later, the numbers are surprisingly unchanged. According to a study by native ad developer Polar, about one-third of native ads don’t meet FTC guidelines for native ad disclosures, according to an analysis of 137 ad units on 65 publisher websites.

“Regardless of the medium in which an advertising or promotional message is disseminated, deception occurs when consumers acting reasonably under the circumstances are misled about its nature or source, and such misleading impression is likely to affect their decisions or conduct regarding the advertised product or the advertising,” the agency said when it released the native ad guidelines in December.

The report also studied native ads that complied with the FTC guidelines and determined which labels to be the most effective. Native ads labeled as “promoted” achieved the highest click-through rate (CTR) at 0.19 percent, while “sponsored” reached 0.16 percent and “presented” hit only 0.12 percent.

With ad blocking on the rise, it’s a reflection of a changing attitude toward intrusive and uninteresting advertising. However, with 408 million people using ad blocking software as of March 2016—a 90 percent growth (nearly double) from last year, even well thought-out ads go unseen.

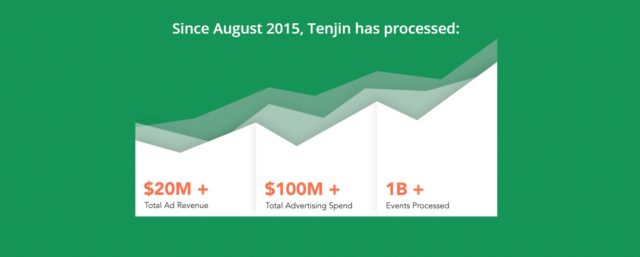

For a marketer, one of the greatest things about mobile advertising is the sheer amount of data you can get about your advertising efforts. Coincidentally, that’s also one of the hardest parts about dealing with mobile advertising—deriving good information and actionable decisions from that flood of information. That’s where mobile marketing and advertising technology firms have stepped in to help marketers deal with Big Data. One of these firms is Tenjin, which promises to streamline mobile marketing and help “spend smarter with our unique growth infrastructure program.”

Amir Manji, Tenjin founder and CTO

As Tenjin co-founder and chief technology officer, Amir Manji describes to [a]listdaily, “We collect and organize data for mobile marketers. We try to help app developers find an audience for the app and evaluate how well their campaign is doing. Typically today, if you’re an app developer, you’ll be spending money and acquiring users through a bunch of different channels, and it’s a big headache to take the data that’s coming in from all those different channels and do an apples-to-apples comparison of them. We try to make that as simple and foolproof as possible.”

Getting data is one thing, but making that process easy and presenting the data in a clear, understandable fashion is another. Tenjin understands the importance of providing marketers with both of those qualities. “We focus a lot on ease of use and simplicity,” Manji said. However, that’s not the key feature that sets Tenjin apart from other martech firms. “Our biggest differentiator is [that] we give app developers access to the raw data,” Manji noted. “We have an app called Data Vault that allows them to see all the data that we’ve collected and organized for them. Then they can take that data and do their own analysis on top of that. Other companies will just have a dashboard where they present some insights to developers. We allow developers to look at the raw data behind the scenes and manipulate it themselves to see what’s going on.”

Of course, the more sophisticated a publisher gets, the more they want to customize the kind of data they get and how they access it. Manji is well aware of this. “Sooner or later, every app developer gets big enough to justify building out their own data warehouse,” Manji agreed. “What we try to do is provide a standardized data warehouse. At a high-level, app developers all care about the same basic metrics, so we try to provide a baseline data warehouse where everybody answers those basic questions the same way, and they can build their own custom data tracking and analyses on top of that.”

The needs of the mobile marketer are definitely changing. “I think it’s become a lot more data intensive,” Manji said. “A couple of years ago, if you had a big enough budget, you could throw it [the app] around at the major channels like Facebook and Google and that would be sufficient to get by. Nowadays, any kind of larger app developer is going to be pretty sophisticated with their buying patterns. If you’re a small or medium sized developer—if you’re not able to do the same level of analysis as them—your buying is going to be less efficient. You’ll be wasting money trying different channels, and you’re already at a disadvantage because you have a smaller budget to work with. We think a smaller developer that adopts our product and our data warehouse puts them closer to being on an even footing with a larger developer.”

The changing nature of mobile games also affects mobile marketing. The amazing success of Pokémon GO has subverted many pieces of accepted wisdom about mobile games, from how fast they can be adopted to how soon in-app purchases happen, to average revenue per user. “I think we’re going to see some games doing very well for a smaller niche audience,” Manji said. He feels that while some apps may be ubiquitous, it’s harder than ever to break through and have a global breakthrough hit. He does point to one of their smaller clients who has done a series of games based on smaller anime shows. “They’re able to find a vein of gold with these users who are really passionate,” Manji said.

Discovery continues to be a major problem for smaller mobile developers, of course, but Manji has some strategies he recommends to developers trying to get their app noticed. “I see a lot of app developers that spend a bunch of money before knowing if their app is ready for that or not,” Manji said. “I would say that step one is to look at your app, look at your current organic users and see if they are behaving the way you expect and if you are monetizing them enough. A lot of people will just throw a big marketing budget together hoping that that solves their problem. That money will be wasted unless the fundamentals of their app are solid. I would start from there.”

Manji cut to the heart of the matter with the core marketing idea that you really have to understand your target. “Generally what you want to do is figure out the ideal audience for your app, and then run some small experiments targeting those users,” he pointed out. “Don’t go out and make a big splash until you know exactly who your ideal user is. Facebook allows you to get really granular with your targeting. Test your hypotheses around the best users of your apps to figure out who are the best users. Once you’ve figured that out you can start opening up the funnel.”

There are some new opportunities on the horizon that should help mobile game marketers. “A lot of people would jump to ad networks, but Apple is rolling out their own paid search, which should help discoverability,” Manji pointed out. “Granted, you’ll have to pay for it, but it’s better than the Wild West there was before. Google Play has always had their own search ads built in. There’s no better place to find a user than the App Store when they’re searching for an app. That should be a channel for every single app developer.”

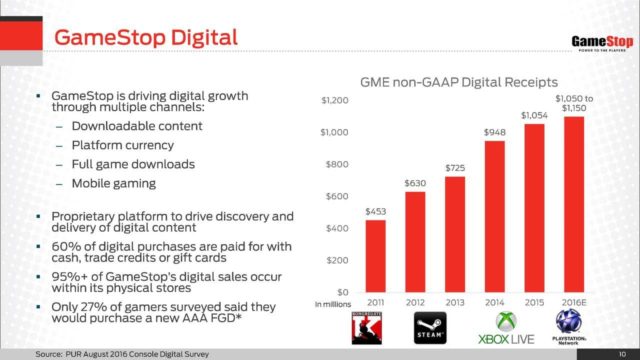

When you want to find out how the console game business is faring, there’s one place you should turn to first: GameStop. GameStop’s market share in the console business is around 35 to 40 percent, which means that what GameStop tells you about console sales is pretty much what’s happening in that market. Paying close attention to GameStop is vital for marketers who want to know what’s happening to the market. GameStop’s most recent earnings call showed a slowdown in sales, but anticipation is high for the quarters ahead.

GameStop’s quarter delivered on earnings per share (at $0.27 per share) but missed on its projected revenue. Total global sales dropped 7.4 percent to $1.63 billion. The big reason fro the drop was the downturn in console hardware and software sales. GameStop “saw declines in hardware of 33.4 percent and in software of 18.2 percent,” said GameStop CFO Rob Lloyd. That led to same-store sales dropping 10.6 percent for the quarter (12.5 percent in the US, 5.9 percent internationally).

Paul Raines, GameStop CEO

“The physical video game business declined again during the quarter with less title count and pre-announced hardware upgrades driving consumer behavior,” said GameStop CEO Paul Raines. “We had anticipated softness in the physical market, but our ability to diversify our revenue and profit stream has allowed us to ride out this cycle successfully.” Essentially, the announcements that both Sony and Microsoft would be seeing new consoles coming out this year not surprisingly caused sales of existing consoles to drop in anticipation of the new hardware.

The more intractable problem for GameStop, which they’ve complained about for years, is the uneven release schedule of major game publishers. When there are strong new releases in a quarter, GameStop does well. When there aren’t new releases, GameStop doesn’t do so well. GameStop also does much better with sales for software that’s being launched. “When we launch games, we typically have 60 percent to 70 percent share during the first week of launch,” Lloyd noted. “Our overall share comes in around 40 percent or so on software. So obviously when a title moves out of that launch phase into what we call the catalog phase, we lose some share.”

GameStop has been changing in order to reduce its reliance on software releases. The company has taken on over 500 AT&T stores as it moves more heavily into what it calls “technology brands,” with notable good results in that area (revenues up 55 percent, contributing 24 percent of total earnings, and strong growth ahead). Beyond that, GameStop is moving heavily into collectibles and licensing, both with its acquisition of ThinkGeek and by cutting its own licensing deals (a Pokémon license for a Snorlax beanbag chair, for instance, which can’t be built fast enough to meet demand).

GameStop is also “creating own reality,” in Raines’ memorable phrase, by working with game studios to publish its own line of games. The first one, Song of the Deep from Insomniac, has been selling well at over 120,000 units so far. “What is interesting is that we have built a complete physical, digital and collectible ecosystem around this intriguing IP working with another great partner at Insomniac games to create a renewable franchise,” noted Raines. GameStop has more games in the pipeline. The thrust of the strategy is clear: “…launching our own IP to take advantage of the gaps in the calendar and the richer margins these games provide,” Raines said.

Good Times Ahead For VR

The prospects for virtual reality (VR) look strong to GameStop. Queried about the prospects for VR this holiday season, GameStop COO Tony Bartel was bullish. “We literally have hundreds of stores that have stations in them, VR stations in them today and in a quarter of our stores we already have had events that have been strong traffic drivers, partnering very closely with Sony, each of our associates are going to be certified in the PlayStation VR,” Bartel explained. “We see tremendous traffic when we run these events in our stores and another element of just how much demand there is, we had the quickest sell-out of preorders in our history the last time we were able to put a PS VR for preorder, we were out literally in five minutes. So there is tremendous demand and in the back half of the year, as people come in, as they talk with our associates they’re incredibly knowledgeable and certified in this, we think it will be a good traffic driver, far beyond the sales that it will generate.”

The latest NPD report underscores GameStop’s information about the drop in hardware and software sales. NPD reported hardware sales for July dropped 30 percent, while software dropped 5 percent. “The lack of strong new releases for the month have resulted with a poorer comp year-on-year, and the top 10 games for July 2016 generated 21 percent fewer dollar sales than they did last year,” said NPD analyst Sam Naji.

Meanwhile, on the digital side of the industry, sales were up 10 percent in July, according to SuperData, reaching $5.9 billion. Mobile games grew by 16 percent, propelled by the success of Pokémon GO, but digital console games and free-to-play PC games both grew by 11 percent. This divergence between physical game sales and digital game sales is not lost on GameStop, which is why the company is continuing to invest in Kongregate as well as its own game IP.

GameStop’s current revenue mix tells part of the story. New video game hardware was $216.4M (13.3 percent of total); new video game software was $382M (23.4 percent); pre-owned and value video game products $543M (33.3 percent); video game accessories $120M (7.3 percent); digital $36M (2.2 percent); mobile and consumer electronics $203M (13 percent); and collectibles $90M (5.5 percent). GameStop is shifting that mix rapidly with its strong growth in electronics, collectibles, and digital products.

The advent of new hardware is a positive thing for GameStop, primarily due to the company’s ability to give people trade-in credit for old hardware to help the purchase of new hardware. Bartel noted that Xbox One S sales showed that 37 percent of the buyers used trade-in credit to purchase the console, no doubt most of them turning in their old Xbox One to get the shiny new Xbox One S. So GameStop is looking forward to new PlayStation models, as well as PlayStation VR and better availability on Oculus Rift and HTC Vive. When it comes time to buy new hardware, many gamers will choose GameStop because they can use old products to get some money off on the new ones.

GameStop sees a bright future ahead. “If we sit here and think about the decline in physical gaming of almost 40 percent from its peak in 2008 and 2016, our strategy of diversification has paid off and allowing us to reach the high end of our guidance this quarter, on our way to a record net income year that we’re forecasting for this year,” Raines said in his closing remarks. “With all the great virtual reality and console expectations coming, we believe physical gaming will return to growth in 2017. In addition, our new growth businesses of digital, mobile and collectibles make GME a very compelling investment for the future as we grow 3 to 5 percent annually to 2019 as we projected at our Investor Day.”

In other words, it’s good times ahead for games—if you have the right product mix and are well prepared for the changing marketplace ahead.

Today, the NPD Group released an announcement stating that it has officially signed an agreement to acquire the video game industry market research and data analysis firm, EEDAR. With the acquisition, NPD (which launched its Digital Game Tracking Service last month) will add EEDAR’s video game database of product metadata, which includes over 200 million facts and 150,000 titles across console, PC, mobile and online/social platforms. Additionally, EEDAR’S GamePulse analytics platform incorporates multiple information sources for contextual insights into industry trends, product performance and marketing strategies. NPD has been the leading source of retail sales data and consumer insights since it first started tracking the video game industry in 1988.

“With NPD’s retail and digital tracking assets, EEDAR’s robust data integration and delivery platform, and our combined industry expertise, we will have the insight and information to grow and change with the industry and drive continued global expansion,” said Tim Bush, NPD president, Americas commercial businesses, in a press release.

Robert Liguori, EEDAR CEO, said in the same press release that: “A fundamental goal of EEDAR has always been to improve the quality and speed by which business decisions could be made for game developers and publishers. NPD shares this philosophy, and the joining of our resources and passion for this sector will ensure the industry has access to the information it needs as it advances into new platforms and business models.”

NPD and EEDAR have a history of collaboration, most recently working together to develop NPD’s Digital Game Tracking Service, which is available in GamePulse. The Retail Game Tracking Service has been part of GamePulse since 2011.

Greg Short, co-founder of EEDAR, spoke with [a]listdaily about what the acquisition means for the two companies. “EEDAR and NPD have been working together in improving insight into the video game industry for our clients for many years,” he said, when asked what led to the acquisition.

Short also discussed how the acquisition would enhance the two companies’ services.

“NPD has global resources, they are the leaders of understanding sales data in the video game space, and they have deep relations across the industry. EEDAR has expertise. We have metadata, which enables the analysis of their sales data at much more granular levels for more interesting trends. And EEDAR and NPD have been collaborating to address the gap of visibility for the digital sales of the industry, in conjunction with leading publishers. We feel that by bringing our two companies together, we have the resources and the expertise that no one else in the industry can bring to bear to finally solve the problem of getting true, accurate numbers about what’s going on in the PC, console, and emerging digital sales areas of the video game industry.”

We also asked if EEDAR would still continue as an independent market research company to serve its clients. “EEDAR will continue to operate as an independent entity. It’ll be known as EEDAR, an NPD Group company,” said Short. “EEDAR will continue to operate, and all personnel are remaining with the company. The leadership and management of the company is remaining unchanged. All of our customers will continue to have access to all that EEDAR has provided, but now with the added benefit of access to deeper resources, a wider range of data and global support.”

“Regardless of the medium in which an advertising or promotional message is disseminated, deception occurs when consumers acting reasonably under the circumstances are misled about its nature or source, and such misleading impression is likely to affect their decisions or conduct regarding the advertised product or the advertising,” the agency said when it released the native ad guidelines in December.

“Regardless of the medium in which an advertising or promotional message is disseminated, deception occurs when consumers acting reasonably under the circumstances are misled about its nature or source, and such misleading impression is likely to affect their decisions or conduct regarding the advertised product or the advertising,” the agency said when it released the native ad guidelines in December.

The needs of the mobile marketer are definitely changing. “I think it’s become a lot more data intensive,” Manji said. “A couple of years ago, if you had a big enough budget, you could throw it [the app] around at the major channels like Facebook and Google and that would be sufficient to get by. Nowadays, any kind of larger app developer is going to be pretty sophisticated with their buying patterns. If you’re a small or medium sized developer—if you’re not able to do the same level of analysis as them—your buying is going to be less efficient. You’ll be wasting money trying different channels, and you’re already at a disadvantage because you have a smaller budget to work with. We think a smaller developer that adopts our product and our data warehouse puts them closer to being on an even footing with a larger developer.”

The needs of the mobile marketer are definitely changing. “I think it’s become a lot more data intensive,” Manji said. “A couple of years ago, if you had a big enough budget, you could throw it [the app] around at the major channels like Facebook and Google and that would be sufficient to get by. Nowadays, any kind of larger app developer is going to be pretty sophisticated with their buying patterns. If you’re a small or medium sized developer—if you’re not able to do the same level of analysis as them—your buying is going to be less efficient. You’ll be wasting money trying different channels, and you’re already at a disadvantage because you have a smaller budget to work with. We think a smaller developer that adopts our product and our data warehouse puts them closer to being on an even footing with a larger developer.”